Friends, I have wanted to (and promised to) write this post for years. While intimidation has kept it on the back burner (investing can be a complicated topic, and I wanted to get it right!), the desire to help and knowing I have something to share has kept it on the stove at all :)

Why? There have been a million articles written on investing, but sometimes you just need to hear it from a “normal person” – someone you trust. I hope I can be that person. Investing doesn’t have to be as intimidating and scary as it can sometimes seem!

So, here we are! My goal with this post is to begin to demystify the topic of investing for the beginner, to tell you a little bit about the difference it’s made in our life, and to give you the push you need to take the next step in your own investing adventure – whatever that might be!

Now is as good a time as any to issue my periodic reminder: I am not a financial planner, and nothing I say here should be construed as financial advice. I’m a gal who loves personal finance, has spent lots of time thinking about it, and wants to pass on what she knows!

Let’s start at the beginning, shall we?

What does investing even mean? Generally, you can understand investing as any tactic or vehicle to grow your money. It usually means assuming some amount of risk. You can invest in things like a CD (low risk), bonds (moderate risk), or an individual stock (high risk). And you can invest through vehicles like 401ks, IRAs, or brokerage accounts.

You can also invest in things like real estate, though for the purposes of this post, we’ll be sticking to financial assets (basically, money).

Why do people invest? Why might you want to invest? Investing allows you to harness the power of compound interest, which is putting your money to work for you – yes!! And when you reinvest your earnings, the pool of money you’re earning interest on grows, which begins a virtuous cycle.

Personally, investing my money is one tool in my financial independence toolkit. The more money I have (to a point), the more freedom I have throughout my life – to make decisions about how I live and give. This is motivating to me. And as a Christian, I believe it’s a part of stewarding what I’ve been given well.

Finally, on a very practical level, most of us need to save for our retirement. A common benchmark is that you should have 10x your ending salary saved if you retire at 67 (you’ll likely need more if you retire earlier). This is nearly impossible to do with the rate on a savings account (you’d have to save SO MUCH!), which is where investing helps you turn time into money (a.k.a. makes your money work for you).

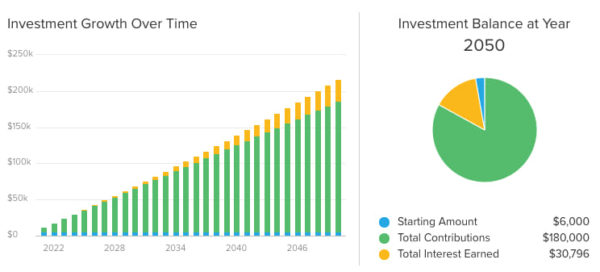

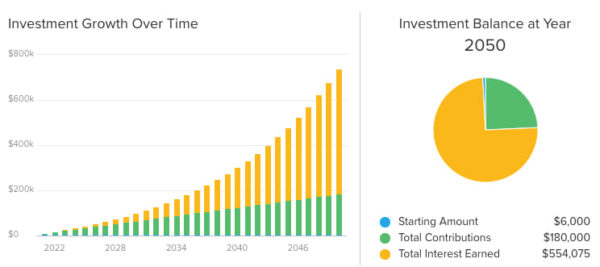

The graphs below illustrate this clearly: the top one shows a growth rate of 1% over 30 years, and the bottom shows a growth rate of 8% over 30 years. The ending balance is wildly different ($216k vs. $740k), and all of that difference is due to interest earned. Both go up, but you’re doing almost all the work in the first scenario.

Do I have to know a lot about investing to be successful? Good news – the answer is no! HOORAH! And it’s a good thing, too, because most of us don’t have the will, the skill, or the time to be investing experts. If you’ve attempted it, you’ve probably realized it can take a LOT of time and brainpower to research and manage your own investing portfolio. (My hand is very much raised here! There are dozens of things I’d rather spend my time doing than researching investments and investment strategy!)

So, how to be successful? Here’s the key: you have to embrace the fact that you’re a novice, and make choices to safeguard against your weaknesses. You’re looking for something that will construct your portfolio for you, and manage it on an ongoing basis. Here are three options:

Option1: A target date fund. If you have a 401k through your work, you’ve probably encountered this investment vehicle before. They’re an extremely common offering in plans because they’re simple and they prevent big mistakes, ha!

A target date fund is an entire diversified portfolio (US stocks, international stocks, bonds, etc.) in one package. It knows when you’ll need to start using the money (your target date, or prospective retirement date) and automatically rebalances to become less risky in its investment mix as you approach that date. For example, it might start out with a 90/10 mix of stocks (higher risk) and bonds (lower risk) when you’re 25, and shift to a 50/50 mix in your 60’s. And you won’t have to take any action to make that happen!

If you choose a target date fund, that’s hypothetically the only thing you’d need to invest in! Experts consider them most appropriate for retirement accounts if your retirement is still pretty far away (20+ years?), because they are simple and not individualized to your unique needs. (After all, they only know one thing about you: when you want to retire. They know nothing, for example, about your comfort level with risk.)

This is what I used in my old 401k!

Option 2: A robo advisor. Welcome to the future! :) This is a digital investment service – just a computer algorithm, with no person behind the scenes – that constructs and manages your portfolio for you. To determine your investments, it will ask you a few questions about your situation, preferences, and goals, then split your money across investments. It will automatically rebalance your investments periodically, and may check in with you periodically, too, to see if your situation has changed.

The pros: it is more tailored to you than a target date fund, and it’s low cost since there’s no person involved. The cons: there’s no person involved :) There’s no advisor who’s taken a deep dive into your situation to help you develop a plan to meet your financial goals.

Though most people use a robo advisor in addition to their 401k for retirement savings, we experimented with using one for our mortgage payoff account. (We liked it, but are currently trying something else!) Most large investment firms, like Fidelity and Schwab, and small firms, like Betterment, have robo options to explore. Here’s a place to start!

Option 3: Wealth management. This option (the most personalized) gets you a trusty sidekick for every part of the investing journey! Your advisor will consult with you on the full breadth of your financial life (your goals, tax situation, upcoming life events, desires, preferences, etc.), and then they’ll use that to design and manage a tailored financial plan and investment strategy.

Unsurprisingly, this is the most expensive option because of its comprehensiveness and customization, and there will likely be a minimum amount of money outside of your 401k you need to have available to invest. (This amount varies, but is probably around $250k+, depending on the firm/advisor.) Often, the higher your balance, the lower the fee, so the higher your balance, the more appealing (and useful!) of an option it is.

If you’re ready to go this route, you might start by looking for an advisor wherever your 401k is housed, or ask for recommendations from trusted friends. And look for someone who is certified as a CFP, or Certified Financial Planner, the gold standard in this industry.

WOW THAT WAS A LOT! Just a few more things, friends.

What can I do to set myself up for success as an investor? A few final suggestions:

1. Honestly evaluate whether you have the will, the skill, and the time to manage your own investments. Remember that one of the biggest dangers to your investment success is you! 2. Remember that investing can feel stressful in the short term. Choose a wise strategy that accommodates your weaknesses and strengths and then check in only at designated intervals. 3. Invest consistently, even when the market goes down. That’s when you’ll get the best deals :)

What is the best way to get started with investing?

1. Start now! Start small, if needed! Remember the power of compound interest. 2. If you have a company match in your 401k, start by contributing enough to meet the match. 3. If you’re already meeting the match, consider increasing your contribution. 4. If you don’t have a 401k, consider opening an IRA. If you already contribute to an IRA, consider increasing your contribution. 5. If your retirement goals are on track, consider opening an investment account, an HSA, or a 529 plan and contributing toward another big goal.

Friends, I’d never be able to answer all of your individual questions about investing, but I hope this post has served to demystify the topic a bit. Accessing the power of the stock market has been incredibly impactful even in just our first decade or so of “adult life,” and I know that power will only grow as compound interest continues to work its magic – and I hope the same for you!! I’m most definitely cheering you on as you take your best next step, and would be happy to answer any follow-up questions below! :)

In honor of our anniversary, I have a relationship-themed Marvelous Money post for you today! (Boy, between this and my post earlier this week, I’m sure leaning hard to the unromantic side of married life for anniversary 8, ha!) Today, I thought I’d tell you a bit about our bi-monthly net worth meetings: what they are, why we have them, why we love them, and why they’re incredibly helpful for our financial progress.

What is a net worth meeting?

A net worth meeting is our chance to review our family’s finances in the big picture. We celebrate progress, check in on our financial goals, discuss challenges and opportunities, and do a bit of nitty-gritty budget upkeep. And, as you might have guessed from the name, we calculate our family’s net worth.

We hold our official net worth meetings every other month, usually in the second weekend of the month unless we’re traveling or otherwise occupied. In this season of our lives, they’re held in the afternoon while the kids are resting, or in the evening.

Tell me more about what you do in this meeting.

Well, first John calls the meeting to order, then we take attendance… j/k j/k. “Net worth” sounds very official, but our meeting is not! Generally, we like to get the small stuff out of the way first by entering any outstanding transactions into our budget doc. (We each have responsibility for entering certain cards and accounts into the doc, which we do about every two weeks, but this is an opportunity to catch up as needed and ask each other any categorizing questions.)

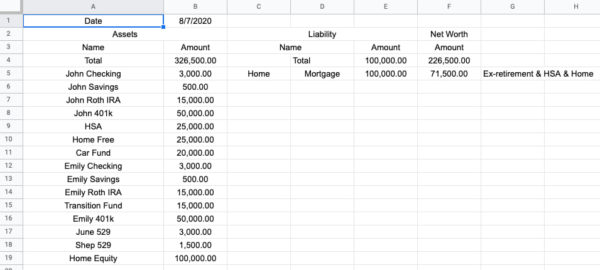

Once the budget is fully up to date, we’ll flip to the “Net Worth” tab of our doc. (For more about the custom Google Doc we use to track our budget, read this post! It’s a bit out of date, but the premise is still the same.) Here’s what it looks like:

Note: these numbers are completely made up, so please do not read anything into them :)

On the left, we’ve listed every single place we have money or an asset. This includes our checking and savings accounts, our IRAs and 401ks, our investment accounts, our kids’ 529 accounts, and our home equity. Yours might include other categories. For us, right now, this is a total of 20 places (I’ve simplified above).

One by one, we log into each of those accounts and enter the current amount as of that date (to be exact, one of us logs in and reads out the totals, the other is the typist). For the home equity line, we simply subtract the remaining principle of our mortgage from the amount we paid for our house to keep things simple. In cell B4, a formula totals everything together – our assets.

In the middle, you can see a column for our liabilities. Currently, this is just our mortgage, but previously we had entries for car loans and student loans. We do the same thing here – log into the account and enter the current number.

All the way to the right, a formula in F4 calculates our net worth – our total assets (B4) minus our total liabilities (E4). We also like to track our more liquid net worth, which for us is our net worth minus our retirement accounts, our HSA, and our home equity. That’s in cell F5.

Next – and this is the highlight of the meeting! – we click over to the tab next door. This tab is called Net Worth Over Time, and for us, it dates back to July 2012 – two months before our wedding, when we began having these meetings! This is what it looks like:

Obviously I have deleted the numbers, though that is our actual chart over the last 8 or so years. This screenshot only shows a fraction of the months we’ve tracked – rows 2-5 scroll and scroll to the right to go all the way back to 2012!

To update this tab, we enter the new numbers for assets, liabilities, net worth, and liquid net worth and then adjust the graph. Generally, it goes up – which is exciting! It’s nice that you’ll see the line go up whether you’re focused on paying down debt or building up savings.

That’s usually the meat of the meeting, but if there’s a challenge or opportunity we want to talk through, this is often a great time to do so. We are comfortable talking about money and it comes up regularly in conversation, so we usually don’t wait for one of these meetings to, say, talk about an upcoming trip or change in our investment strategy, but if you’re newer in the process, using this set aside time for that might be helpful.

Finally, because I know the budget is as up-to-date as it will ever be, I’ll go through it category-by-category to make sure we’re on track for each one, and adjust as necessary (of course, always making sure our total in the ISE is in the black!). Again, for more on how we budget, go here.

Why should I have one of these meetings?

First and foremost, we consider these meetings an opportunity for celebration. They’re a way to recognize the good decisions we’ve made and the willpower we’ve exercised, to cheer ourselves on to do more of those things. Saving money is often not “exciting,” especially over a long timeframe, and so we find it helpful to build in excitement where we can, to keep us motivated for the long haul.

A comment my friend Kelly made years ago on an MM post brought home why this is important. She commented that she often feels like the money she puts into her 401k “isn’t real,” since it’s taken right out of her paycheck and she basically never sees it again. While in some ways this is good (you don’t need or want to be checking in on longterm investments constantly!), you’re also missing out on a chance for motivation if the money you’re saving never becomes real to you. If you see the amount adding up over time, and watch compounding work its magic, you even might be motivated to save MORE!

Second, working toward a goal together is great for a relationship. It gets you on the same team! Whether it’s a money goal or a fitness goal or a trip you’re working toward, feeling unified in the things you want bonds you together. These meetings help with that.

The final and really important reason to have a meeting like this is so that both partners have visibility into the family’s finances. In a very practical sense, they help make sure both partners know what accounts exist, where they are held, how to log into them, and approximately how much money exists and where. No matter how duties are split, everyone should know the basics.

One final point to address: I hope this has been clear throughout this post, but these meetings are not about us counting up our money for the sake of having money. Having money is not evil, but it’s also not the point. For us, the point is freedom – freedom to live and give how we wish, to the best of our ability and for the glory of God. We also believe our money has been entrusted to us, and we want to be wise managers of it. A wise manager checks in and makes adjustments to get the most out of what they have, and these meetings are one way to do that.

Friends, I would love to hear: do you currently have a financial check-in? (And YES, you can totally have one of these if you’re single!) Any questions about our meetings, or requests for a future MM post?

Two and a half years ago, I shared with you our plan for paying off our mortgage early. In that post, I walked you through our journey up until that point, from simply making extra payments each month to investing the extra payment in a brokerage account. Over the last year there’s been a new plot twist (as I alluded to in this post!), and I’m happy to pull back the curtain today!

Let’s look at a timeline, shall we?

Spring 2013: We buy our house! We pull together a 13% down payment. Fall 2014: After paying off our car loans, we use about half of what we had been paying to make an extra mortgage payment each month (directly to the bank), and the other half to build up a fund for our next car purchase. Fall 2015: Car fund complete, we shift the amount we’d been paying toward our mortgage, too. Instead of paying down our mortgage directly, though, we begin transferring the extra monthly amount into a brokerage account and invest it in a mutual fund.*

The main critique of paying off a mortgage early is that it doesn’t make sense to pay off a low interest rate mortgage when you could be earning higher rates of return by investing. We still planned to pay ours off early, but ALSO wanted to take advantage of compounding interest by investing the extra payment instead of applying it directly to the mortgage. We were comfortable with the extra risk that exposed us to (and the extra willpower it required of us!).

When we saved enough to pay off our mortgage, we would pay it in one lump sum. Hooray, right!?

My husband, though. He’s always thinking. And last year, he came to me with a suggestion: what if, instead of simply saving the amount we needed to pay off our mortgage and then handing it over to the bank in one huge sum, we saved a little longer – maybe two or three years, maybe less, maybe more (depending on the market’s performance). If we could wait just a few years longer, then we would have amassed a large enough amount of money that, carefully invested, the returns themselves would be large enough to cover our monthly mortgage payment, meaning our mortgage would no longer need to be a part of our household budget.

It would be as if we had paid off our mortgage, and yet, we’d also be realizing these other benefits:

1. We would not lose the mortgage interest tax deduction (less of an issue under current tax law).

2. By the miracle of compound interest, in 23 years, when we make the actual final payment, our calculations project we should still have anywhere from 50% to 150% of the money we started with (!!!).

3. That large remaining lump sum could then be used to pay for kiddo college tuition, a rental property, a fabulous vacation, some really extravagant generosity, or – most likely – all of the above.

A mostly unrelated but highly adorable photo of Shep and our home

When John first presented this plan, I was not particularly enthused – all I heard was “a few more years of saving” and no “we’re debt freeeeee!!!” scream. (Because technically we wouldn’t be, and it would be weird to scream “we have XXX in our bank account!!!”)

But John’s desire was to make the most of our years of sacrifice, because we both desire to be good stewards of our money. This sounds harsh, but to work so hard to save so much and then sink it directly into a illiquid asset like a home instead of allowing it to continue to grow seemed like a squandering of possibility. If we could steadfastly reach this goal at a relatively young age, it would behoove us to continue that momentum instead of slamming on the brakes by sinking it into our home.

Okay – I was on board. And maybe you’re nodding alongside me right now. This all sounds good, right?!

Here’s the HUGE X factor – with this iteration of the plan, like the last one, we are vastly more exposed to the market than we would be if we were making payments directly to the bank each month. As I talked about in this post, by making those payments directly, it’s like getting a guaranteed 4% (or whatever your mortgage interest rate is) return – nothing thrilling, but respectable for zero risk. Our approach requires accepting that the money we’re socking away could actually lose value – and that’s why we don’t know exactly how long it will take us to reach our goal.

Worth mentioning at this juncture: if you like the idea of trying something like this, I would highly recommend working with a financial advisor (and one who understands what you’re trying to do). Of course, it’s possible to make investment decisions on your own, but I don’t want to give you the impression that it’s just little Miss Creative Director over here knowing all the things and that you should be able to do the same. John IS a financial advisor, and if he weren’t, we would definitely be seeking expertise on decisions of such magnitude.

A final word of caution, the same one I gave in my last mortgage post: I would only consider doing our “next level” system if you have a long track record of steely willpower with your money. It is so tempting to just take a little here or there as you watch that fund grow and other needs come up. If you’re nervous you’d be tempted or don’t want to stomach the risk, just apply the extra payments straight to your mortgage – done and done. Also a fantastic option.

I want to end by saying I realize this post is Marvelous Money 301. It’s a more advanced topic than I usually touch on, and perhaps it feels wildly out of reach for you right now. I get that. I share this not to brag (!!!) or make you feel defeated (hopefully you know that!), but to stretch your imagination of what’s possible, and perhaps plant in you an idea that you’d never heard of before.

My next MM post (series!) is going to be squarely back at the 101 level, and it’s the most-requested topic that I’ve yet to touch on: investing 101! I can think of few topics that are simultaneously as intimidating and as powerful. I’m excited to dig in :)

*Earlier this year, as an experiment, we shifted our money from mutual funds into a managed account. We’ll talk about this more in the forthcoming investment series!

A final reminder: I am not a financial professional, and nothing I say here should be construed as investment advice! I’m just one gal sharing her story :)

If money doesn’t make you happy, you’re probably not spending it right.

Of course, money on its own will never satisfy, and it will never fill the deep well reserved for God and people. But spent thoughtfully, within a budget, and according to your values, I believe your purchases can and should make you happier. (After all, even the quotidian stocking up of paper towels still gives me a brief buzz of adulting joy!)

But, looking back over my decade-plus career as the manager of my own purse strings, there are certain items that I still look back on, years later, and think to myself, “I am SO GLAD I spent money on that.” Here are ten of them. I hope my list encourages renewed gratitude for your own favorite purchases, and with your list in front of you, see if you can find any common threads in what you value most highly – and then let those threads guide your future purchases!

In no particular order…

1. Our tan sofa. We bought our sofa from Macy’s in 2011 for $700 delivered, about a year after John got his job. Before that, our living room contained one seating option – our white loveseat from Ikea, purchased midway through college. This purchase represented one of our first big leaps into adulthood, and we saved for months and months to afford it. It is incredibly comfortable, the velvet fabric is impervious to stains, and the practical color hides the dust of daily life effectively. It still looks fantastic after eight years; we hope to have it for many more.

I chuckle when I think about a sweet reader’s comment I got many years ago – something along the lines of, “wait until you get rid of that brown couch – then your room will look really good!” Though you could read it as rude, it didn’t bother me at all. I just thought to myself, “sister, if only you could sit beside me on this here brown couch, you’d know why I’m never getting rid of it” :)

2. Our dunes painting. My wedding gift to John was an original painting I found in a small shop in our Connecticut hometown in 2011. It already had a lovely frame, and I think the price was about $400. It was more than I had budgeted for his gift, but the moment I saw it, I fell in love – it reminded me of his beloved Michigan dunes. I loved the idea of his wedding gift being something we’d keep forever, as opposed to a piece or clothing or an accessory he might wear out. I also felt VERY grown-up purchasing an original piece of art, and there was something sweet about finding his gift so unexpectedly in our tiny hometown, the place where our story began many years before. The painting now hangs on our bedroom wall.

3. My dresser. In 2014, I spotted a low, cream dresser an acquaintance was selling on Instagram. Maybe it was the way she had merchandised it (she’s a photographer!), but I instantly knew it was a piece I’d love for a long time. At $200, I also knew it was a steal. Taking full advantage of our fun and fancy-free pre-baby life, we rented a truck from Home Depot and drove over to Greensboro to bring it home (out-of-nowhere rain storm on the way home and all!). It took ALL of my might to get my end up our front steps (that sucker is HEAVY), and it’s lived happily in our master bedroom ever since. It’s the kind of piece that could look good anywhere, and I plan to have it forever (not the least because I never want to move it again). Peep it in the background here.

4. Our mattress. Late in 2014, John convinced me to get a King-sized mattress. I was opposed to the idea at first – why would he want to be further away from me?! – but eventually gave in. We trotted down to our local Mattress Warehouse and tried out all the options in the store, finally settling on one we both loved after a good hour of reclining on various options. The price – $1,600 – was a little more than we had been planning to spend, but we were confident this was the one for us.

We called the salesperson over. He looked at the tag, and then did a double-take. He explained that there had been a mistake, that the tag on our mattress had been switched with another one and that our mattress was actually supposed to be $2,500. After confirming with his manager, however, he graciously honored the price and let us take ours home for the lower price.

Now, I don’t know if this was some sort of elaborate sales technique to make us think we got a great deal. (Kudos to them if it was!) What I do know is that pretty much every night since, John and I have looked at each other before turning out the lights and said, “I love our bed.” Given the importance of a good night’s sleep and based on how much we love our mattress, I’d have gladly spent $2,500 on it… but I’m glad we didn’t have to :)

5. Our laundry baskets. 2014 was a big year for beloved acquisitions! There are a number of reasons that could be so, but here’s one: in 2014, we had recently paid off my student loans, were rapidly making progress on our car loans, and were looking forever to putting our full efforts toward our mortgage. Every dollar was aggressively scrutinized; if one was going out the door, you can bet it was for something we were all in on.

Which brings us to our laundry baskets. I spotted them at Home Goods on Black Friday, and even though I remember hesitating over the price ($50 for 2!), I brought the wicker pair up to the register. Like several other purchases on this list, there was just something that spoke to my soul about replacing our mismatched college bins with a matched, grown-up pair. We use and love them to this day.

6. My favorite jeans. I wrote an entire post about these jeans, so you know they’re beloved. In the throes of post-second-pregnancy life, the angels sang when I slipped them on. Great quality, the right amount of stretch, a fab high waist, denim that feels SO GOOD on, and a more-than-fair price point (I got mine for $60 on sale!). Confession time: I wear them 5/7 days a week, emailed customer service to request they make a white version, and have convinced a handful of friends and family members to buy their own pairs. Maybe you’re next? :)

7. My first car. Maybe it’s on the list because I was really hoping for an SUV but thought I could only afford a sedan. Or maybe because it was incredibly comfortable, the best road trip companion for my many trips around the South. Or maybe because it was, after all, my very first car, and negotiating its purchase on my own is one of the most grown-up things I’ve ever done. For whatever reason, my Mariner will always be one of my most beloved purchases. I would happily still be driving it today if the transmission hadn’t died the last time we were in Michigan – see above for our farewell family photo!

8. My leopard-print gloves. At $5 from Walmart, purchased while still at college, these beauties win the “most bang for my buck” prize by a landslide – especially considering I’ve worn them every winter for approximately the last twelve or so years. With holes in several of the fingertips, my family likes to joke that these were my texting gloves before texting gloves existed. They’re simple, they’re chic (well, aside from the holes), and when I find something I love, I tend to wear it into the ground.

9. Our TV console. A newer addition to the family, our console joins the list because it solved a problem I had been puzzling over for more than a year. With one fortuitous trip to Home Goods, it brought style, organization, and a much-needed additional surface to our living room in 2018. I searched every retailer known to man for more than a year, almost pulling the trigger on pieces three times as much as this one ($430) multiple times, but I am SO happy I didn’t settle for something I didn’t love.

10. Our Le Creuset. Last but certainly not least is our Le Creuset dutch oven. Back in February 2012, we were throwing our very first dinner party together – a Julie & Julia themed event for four couples with boeuf bourguignon on the menu.

Needless to say, we were anxious new hosts, and in a spontaneous flurry of nerves, we decided we needed this exact pot on the morning of the party. We dropped $140 on it like it was nothing, which makes me laugh to this day – because $140 was most definitely NOT nothing at that time in our lives, and nothing but the nervous desire to have everything go right for this big event could have made us make this sort of spur-of-the-moment purchase. Happily, we have used this very pot to cook thousands of meals since, and considering it’s Le Creuset, I’m confident we’ll use it to cook thousands more – and smile every time we remember the reason it joined our family :)