Marvelous Money: Why save for retirement?

Welcome back to Marvelous Money! We appear to have taken a bit of a summer hiatus, but we’ll just call that time to let the first seven posts sink in. (Missed one? You can find them all here.) So far we’ve covered emergency funds, managing joint finances, building a budget, and yes, how to spend money :) Now, it’s time to talk retirement.

Before we get into the nitty gritty, though, I thought it might be worthwhile to spend a bit of time on the WHY. Or, perhaps more importantly, the why NOW.

Because yes, everyone knows that theoretically they should be saving for retirement. But are you? I’m betting that if you see the reality of what starting now versus starting in ten years means for your future, you will indeed be motivated to take action. If you’re reading this in your twenties or thirties, you have an insane amount of power in your hand, and it’s called compound interest.

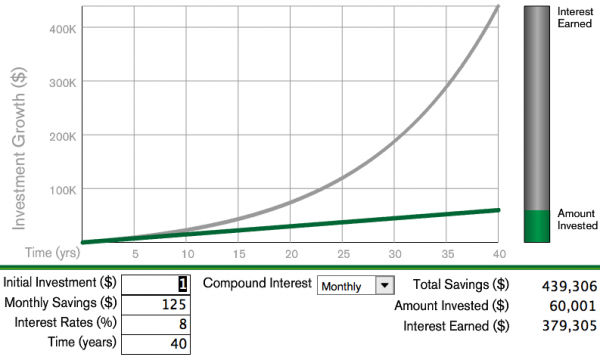

Let’s look at a few numbers. Let’s say you start saving for retirement at age 25. You put away $125 a month, and you earn an 8% average every year (around the average annual historical return of a balanced portfolio of stocks and bonds). After 40 years, at age 65, you have about $439k. Marvelous!

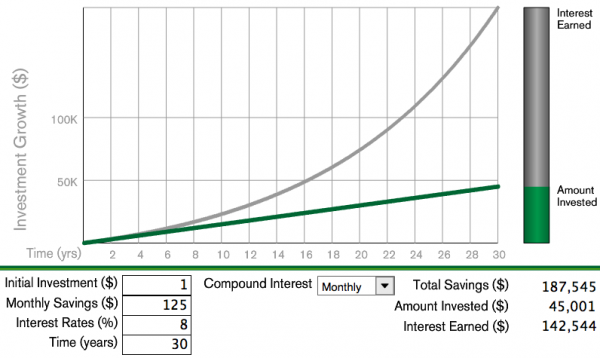

Now, let’s say you start saving $125 ten years later, at age 35, with the same return. At 65, you have about $187k.

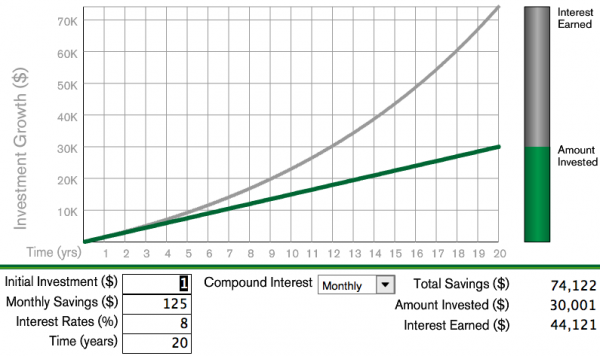

Let’s go one step further, starting at age 45 and saving $125 a month. At 65, you’ll have just $74k. Yipes!

Obviously, if you start saving later in life, you’d probably save more per month — if you can. But WE want to make our money work for us, don’t we? And I don’t know about you, but I think the demands on my money are only going to grow as I get older.

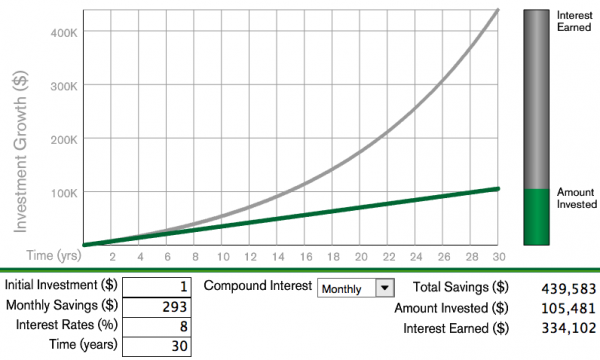

To go back to our example for a moment, let’s say you start saving for retirement at age 35 but want to end up with the same amount of money at 65 as the peeps who started at 25. To start ten years later, you’d have to save MORE THAN DOUBLE the amount per month — $293 versus $125.

This gets at the question I pose in the title of this post: Why save for retirement? Fully funding your retirement means setting yourself up for financial independence. Not only will you have more flexibility later in life (when to retire, etc.), you’ll have more freedom throughout your life, as you need to save less money to reach the same goal.

Just one more example. Imagine you’re given two options: you can have one million dollars today, or a penny that doubles in value every day for a month. Which do you take? If you take the penny, after the first ten days you’ll have $5.12. Not too exciting. After 20 days, you’ll have $5,242.88, which is better, but still nowhere near one million. BUT WAIT, there’s more — by day 28, you’ve surpassed the first option with $1.34 million, and on day 30, you have $5,368,709.12. Marvelous, indeed!

The lesson? You can’t skip the boring part — and I guarantee saving for retirement might look boring for awhile. But the boring part? That’s your ticket to the exciting part, where your money truly starts working for you. The most growth comes at the very end.

So, here we are. You have to start. Time is the most powerful part of this equation, and it’s the ONLY part you can never make up. I know that there are lots of demands on your money, and maybe $125 a month seems like a lot right now. However, if you read this blog, I would be willing to bet that you’ve been spending $125 per month on something discretionary that you could redirect toward retirement savings. Fun? Nope, not always. But I don’t expect anyone to hand me my retirement, and I don’t think you should, either. As my Dave Ramsey friends like to say, if you will live like no one else, later you can live like no one else. And that’s the truth.

Much more to come on this topic in the coming weeks, but in the meantime, I would LOVE to hear from you. Where are you right now with retirement savings? Do you have a 401k or IRA? Do you contribute a set amount per month or year? Do you feel good about where you are? This will be super helpful as I plan future posts, so please chime in, friends!!

P.S. Since I’m asking you to share, I should, too: I opened my first IRA at age 19 (traditional) and opened a Roth a few years later. I’ve contributed a bit less than $125 per month over the last few years since we were focused on debt reduction, but the big goal for 2014 is to fully fund! More on all this soon!

I’m very lucky in that my parents opened a Roth IRA for me when’s was 16 and helped me contribute to it. Now I do it on my own, but I feel so lucky that I got a head start on it! I definitely think you should discuss what a Roth IRA (and traditional and a 401k). So many people don’t know what they are and how easy it can be done!

@Liz Yes, ma’am! Definitely important and we will definitely cover!

I love these posts and as a business owner and being self-employed, I am pretty clueless about 401k’s, Roth IRA’s, and all things retirement. But, I know that means its even more important as someone self-employed that I understand more about retirement since I don’t get those benefits through an employer. I’d love to hear more about the difference and where to even start if you’re clueless like me!

I have been taking advantage of my company’s 401k plan. They match 75 cents of every dollar you put in, up to 10% of your paycheck. It has definitely helped me start saving early, plus it’s free money!

I have to agree, I was pretty clueless (and still am) about all the different IRA’s and funds you can set up for yourself. I really enjoy reading about money management, so I look forward to more in the future :)

I adore these marvelous money posts! I even have my boyfriend who is a financial planner reading them and we both agree you use great examples. Thank you thank you!

my employer matches up to 4% in a simple IRA so I take advantage of that. I never otherwise would have probably started but I’m so glad I did when I was 23… although it doesn’t seem like a lot now I know it will add up and end up to be a lot more than I expect… plus, as Miranda said, FREE MONEY! I think a big part is having it automatically taken out, if it were up to me I would have a hard time deducting that money every month.